Let’s say you want to be a great gift-giver. If you do, you need to 1) desire the best possible life outcomes for your recipient and also 2) recognize that you don’t exactly know what that best outcome is.

With a healthy regifting economy, gifts flow to their most efficient uses.

All gifts, like all capitalistic ventures, require some risk and leap of faith that you have found the solution to a problem for your recipient, despite all the unknown variables.

It’s also true that most gifts, like most capitalistic ventures, fail to do that.

You should encourage your recipient to feel free to regift your presents. An oven mitt which is useless to Sally (who already has an abundance of oven mitts) may be a perfect gift for her friend Sue (who is just getting started with cooking). One man’s trash is another man’s treasure. Our social stigma against regifting would leave Sue without a good oven mitt and leave a good oven mitt gathering dust in Sally’s kitchen drawer.

With a healthy regifting economy, gifts (like goods and services) flow to their most efficient uses.

You might tell me that regifting is bad because of a loss of symbolic value when you regift something. “It’s the thought that counts,” you might say.

I’m none the poorer for her having given my gift away, and she is actually better off having done so.

I’m not suggesting that you take the positive thought or intention out of your gifts. I’m suggesting that your intentions should include the possibility that regifting and trade is actually a good thing for the recipient, too.

I gave my sister-in-law a bag of coffee beans for Christmas this year. It turns out coffee is not her thing (I didn’t know this), so I encouraged her to re-gift to her colleagues. Coffee beans are a great professional gift, and good professional gifts are great for building social capital and rapport.

She ended up giving the coffee to my Dad, which happened to be a great trade: he had just gotten a coffee bean grinder that same morning. This is a great example of the calculations involved in a regifting transaction. I’m none the poorer for her having given my gift away, and she is actually better off having done so.

In recent years, various scholars have revisited Adam Smith, finding much more in his work than the homo economicus obsession with self-interest. That effort raises important questions — specifically, how might economists incorporate such other moral values as empathy, regard for others, and altruism?

Schapiro and Morson believe that both the humanities and economics could contribute much to the other. The humanities have become too arid and formalistic, they argue; economics has become too “mathematical” and focused on what can be measured than what should be achieved. Their objective is to encourage the unification of the two fields — a Herculean task, certainly, but they take some first steps in that direction.

They criticize economists for arguing that economics alone can resolve policy questions laden with ethical concerns.

Importantly, they recognize that Adam Smith, in The Theory of Moral Sentiments, values the human trait of empathy as equally important to the trait of self-interest he so well explains in The Wealth of Nations. But that emphasis leads them to view these two traits as distinct and conflicting, rather than as interrelated and complementary. Thus, they neglect the ways in which capitalism and its key institution, the corporation, integrate these two traits. A firm must focus on self-interest — how else can it survive? But its employees and managers must also become skillful at “reading” others, at developing the empathetic traits, essential to crafting win/win, mutually beneficial arrangements with its economic partners.

Morson and Schapiro cover an array of ethical issues but give economics greater attention. Specifically, they criticize economists themselves for arguing that economics alone can resolve complex policy questions laden with ethical concerns.

They agree that economics can help managers achieve greater efficiency in achieving their goals; however, they note that the emphasis on analysis and quantitative goals can lead to a neglect of ethics. “Efficiency to achieve what?” is their question. Economists, they assert, have become too “imperialistic,” too quick to convert everything into a quantifiable and solvable equation. But they also note that the humanities have been affected by post-modernist trends, even as they seek to outdo economic imperialism by quantifying the unquantifiable. Their point is that the push toward “scientification” has impoverished both fields, that each should reach out to the other to bolster their capacity to consider ethical questions.

Ethics Are Not Quantifiable, Numbers Are Not Empathetic

While agreeing that complex tradeoffs are involved, they note that too often the ethical issues are ignored.

The utilitarian bias of much economic analysis is certainly ripe for criticisms and Morson and Schapiro add to the work of Deidre McCloskey and others on that score. To illustrate their thesis, they look at an array of policy areas where economics provides a strong focus — admission selection criteria for colleges, markets for kidneys and other organs, and how poor countries might best develop (including a very good review of capital, institutions, technology, and culture). They argue that, while economics often provides guidance on how to “efficiently” address such problems, too often it runs the risk of failing to attain richer and more ethically grounded, but less readily quantified, objectives.

Their example of college admissions provides a detailed discussion. The authors — both full professors and one the Dean of Northwestern University — are well equipped to address that area. They understand the costs of over- or under-fulfilling enrollment goals. However, they warn that too often admissions officers neglect the moral and ethical challenges that prospective students face. Is it ethical for colleges to use variable pricing based on a student’s likelihood of acceptance to provide them less financial aid? Businesses, of course, use diverse price levels of necessity, but should colleges? Is their goal to educate or maximize their students’ lifetime achievements? And if so, is that interpreted in earning potential or some other metric?

While agreeing that complex tradeoffs are involved, they note that too often the ethical issues are ignored. They suggest that while university spokesmen claim to speak with moral authority, their marketing policies are more akin to those of used car salesmen.

Not Always On-Point

However, when the authors turn to areas outside their core competency, their discussion is less insightful. The discussion of the ethics of allowing markets for organs, kidneys specifically, recognizes the limits of donations based on familial or friendship ties. Tens of thousands of individuals in need of kidney transplants remain on waiting lists every year. They discuss some innovations — such as chain donations that give a donor the right to a kidney for themselves in the future — and they recognize that allowing compensation might eliminate the deficit. But they worry (as do scholars such as Harvard philosopher Michael Sandel) that confronting individuals, especially the poor, with such market choices creates avoidable ethical challenges.

A true understanding of Smith’s insights — and capitalism itself — requires a larger perspective.

What “should” or “should not” be in the market — from payday lending to kidney transplants — is an ongoing debate, but I do not view that as a conflict between an ethical and a utilitarian choice. Rather, such “economic” transactions, being cooperative and benefiting both parties, are also altruistic.

Morson and Schapiro seem to realize this point, at least in part. In their chapter, “De-hedgehogizing Adam Smith,” they note that Smith wrote extensively about ethics in The Theory of Moral Sentiments, arguing that self-interest, a trait critical for human survival, is balanced in social interaction by the other-regarding trait of empathy, or “fellow-feeling,” and that the market is made possible only by the creative synthesis of these two traits. Competition provides the discipline to keep the two traits in balance. Both are necessary for the creative voluntary system of wealth creation that is capitalism in practice.

A true understanding of Smith’s insights — and capitalism itself — requires a larger perspective. Thus, a dialogue between two large and complex fields of knowledge seems a useful, though difficult starting point. Still, this book may still encourage others to open the door to a broader understanding of the morality of markets and capitalism. On those grounds alone, it merits attention.

Fred L. Smith, Jr. is the founder of the Competitive Enterprise Institute. He served as president from 1984 to 2013 and is currently the Director of CEI’s Center for Advancing Capitalism. He is a member of the FEE Faculty Network.

This article was originally published on FEE.org. Read the original article.

A recent report from Stanford University’s Hoover Institution details the “Hidden Debt” and “Hidden Deficits” contained in state and local government pension unfunded liabilities. The report begins by stating:

“despite the introduction of new accounting standards, the vast majority of state and local governments continue to understate their pension costs and liabilities by relying on investment return assumptions of 7-8 percent per year. This report applies market valuation to pension liabilities for 649 state and local pension funds. Considering only already-earned benefits and treating those liabilities as the guaranteed government debt that they are, I find that as of FY 2015 accrued unfunded liabilities of U.S. state and local pension systems are at least $3.846 trillion, or 2.8 times more than the value reflected in government disclosures. Furthermore, while total government employer contributions to pension systems were $111 billion in 2015, or 4.9 percent of state and local government own revenue, the true annual cost of keeping pension liabilities from rising would be approximately $289 billion or 12.7 percent of revenue. Applying the principles of financial economics reveals that states have large hidden unfunded liabilities and continue to run substantial hidden deficits by means of their pension systems.”

Chart via Hoover

By using unrealistic investment targets and only reporting the earned benefits as liabilities, the public pension system under represents the complete picture of its unfunded liabilities. As of fiscal year 2015, the complete accounting for unfunded liabilities from all cities, states, governments were $1.378 trillion. This is after recently implemented governmental accounting standards. Nevertheless, these accounting methods do not incorporate more market valuation techniques which treat future obligations as a capitalized long term debt. This problem arises because recent reforms in governmental accounting permitted pensions to assess their liabilities based expected return on assets. Thus, there is little allotment for the inherent risk posed by these projections. Especially, when pensions place expected rates of returns at 7.6%(a expected rate return that is proving difficult to obtain) which would mean that they expected the value of their money to double approximately every 9.5 years. These projections create distortions that under state the true cost of the unfunded portion of the pension liabilities. According to the report:

“The market value of unfunded pension liabilities is analogous to government debt, owed to current and former public employees as opposed to capital markets. This debt can grow and shrink as assets and liabilities evolve. From an ex ante perspective, the economic cost of the pension system to the sponsor is the present value of the increase in pension promises (service cost) plus the cost incurred because existing liabilities come due a year sooner (interest cost). Under lower discount rates, the service cost is higher but the interest cost is lower.”

Fitch has adjusted the expected discount rate for public pensions to 6% from the rating agency’s previous 7% expected rate of return. This change is based on what the rating agency views as slowed economic growth that will adversely affect investment returns for public pension funds– a possible repeat last year investment earnings decline seen by public pensions.

According to a source in the agency, the US economy has been exhibited signs of sluggishness. That does not bode well for investment performance. Public pensions are eager to maintain returns in order to lessen their future liabilities. Nevertheless, the current market environment does not appear to lead itself to the capturing of easy returns. For public pensions, this will result in the potential increasing of future liabilities. Estimates place the expected increase of future liability public pensions at upwards of 11%. Public pensions will either have to increase the amount of contributions to the funds or decrease the expected payouts. Both actions would be advisable but will undoubtedly cause consternation among public employees.

Shifts in the aging population could have impacted the current economic picture. As baby boomers continue to retire, work force participation is certain to decrease which will affect the overall market. The elderly are also living longer. Actuarial updates for public pensions will be required to reflect these changes. Currently, the define benefit plans that are offered to public employees do not appear to be sustainable as many struggle with underfunding, violate market environments, and increased number of participants requiring payouts. In order to combat this, the pension system have invested in a more diverse range of equity, fixed-income and alternative assets- a reaction to today’s low interest rate environment. Nevertheless, such investment strategies are bound to increase volatility with the possible result being the unintended consequences of lower investment returns. Thus, this has the potential to further exacerbate the already stressed public pension system.

No simple solutions are readily available. And one can make an argument that the current discount Rate For Public Pensions should be cut even further.

Last week it was reported that the illinois Budget was in dire financial straits making it a perfect candidate for Sate Bankruptcy. The state faces $15 billion in backlogged bills and mounting ratings downgrades from credit agencies. The struggling state is poised to obtaining the dubious honor of being the first state to be rated junk status in US history. Traders have responded in kind sending the yields on Illinois bonds higher-a reaction from court orders that claim the state violated previous orders and must adhere to prior obligations to vendors.

The State has yet to pass a budget for the last three years – the longest for any US state- and has recently announced via its Transportation Department that roadwork would stop starting July 1st. The Powerball lottery is also considering dropping Illinois over its lack of a budget. Compensation to state employees is in jeopardy of evaporating. According, to a recent piece from the Associated Press, the state Comptroller Susan Mendoza is sounding the alarm regarding the turmoil the financial strapped state is facing. The piece explains that court ordered lawsuits by state suppliers are binding but the state’s monthly revenue isn’t enough to meet these obligations. This puts services such as school buses and ambulance services at risk of shut down.

In the state legislator, both parties are battling over the finances of the state. The Governor, Bruce Rauner, has been adamant about instituting changes to the budget before supporting any tax increases. Democrats in the State argue that his demands like term limits for lawmakers, a four-years property tax freeze, and new worker compensation laws would hurt working families. Such arguments will fall on deaf ears as the State increasingly faces the harsh reality of mounting bills coming due. State suppliers and vendors are increasingly lining up to file lawsuits against the state demanding payment. Recently, The administrator for the State’s Medicaid program went to court to obtain a order for $2billion of unpaid bills. The city is running out of time and drastic measures are needed urgently for the Illinois budget. “Once the money’s gone, the money’s gone, and I can’t print it,” Mendoza said.

Even if the mention of a “Gold Standard” makes your eyes glaze over, the video above and the article below show you how a monetary system SHOULD WORK. More importantly, you learn how the US can extract itself from ever-compounding debt. Currently, the FED is destroying savers in the name of “helping” the economy. Learn how credit can expand and contract WITHOUT booms and busts.

Get our full guide on Phil Fisher in PDF

Get the entire 10-part series on Phil Fisher in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues.

The choice of the word “unadulterated” is not accidental. There were many different kinds of gold standard, including what we now call the Classical Gold Standard, the Gold Bullion Standard, and the Gold Exchange Standard. Each contained flaws; each was adulterated.

For example, in the Coinage Act of 1792, the government forced the price of one thing to be fixed in terms of another thing. The mechanism was in Section 11:

“And be it further enacted, That “the proportional value of gold to silver in all coins which shall by law be current as money within the United States, shall be as fifteen to one…”¹

Of course, people respond to such distortions. When the government fixes the price of something too low, then people will hoard or export it. If the price is fixed too high, then they will flood the market with it.

According to Craig K. Elwell, in his 2011 Congressional Research Service Report:

“Because world markets valued them [gold and silver] at a 15½ to 1 ratio, much of the gold left the country and silver was the de facto standard.”²

Subsequently, the government changed direction. Elwell notes:

“In 1834, the gold content of the dollar was reduced to make the ratio 16 to 1. As a result, silver left the country and gold became the de facto standard.”

If the law dictates the ratio between gold and silver, then only one metal–the one that is undervalued–will be used. It would be extremely difficult for the government to get the ratio exactly right. And even if so, as soon as the market value changed the ratio would be wrong and only one metal would circulate.

The government should not attempt to force a price onto the market. In the unadulterated gold standard, the market is allowed to set the price of silver, copper, oil, wheat, a fine wool suit, and everything else. It allows people to use gold, or silver, or seashells as money if they wish (the market has not chosen seashells in modern history).

Throughout the 19th century, there were various state laws to impose new kinds of restrictions on the banks. One popular restriction was that in order to obtain a charter (permission to operate as a bank), the bank had to buy state government bonds. This theme–forcing banks to buy government bonds–was to recur later.

This is a pernicious idea. Banks must have an earning asset to match the liability of the deposit accounts. Why not make them buy some government bonds as a condition for permission to operate? Because this is obviously blackmail. In a free country, one should not need to ask permission to be in business and one should not be forced to do something in exchange for that permission.

This policy has two economic effects. First, it pushes the price of the government bond higher than it would otherwise be, which means it pushes down the rate of interest. This distortion ripples throughout the entire economy.

Second, it exposes the state-chartered bank to the fiscal irresponsibility in the state capitol. And of course the state capitol is encouraged to borrow and spend by this very perverse policy, because they know that there is always a market for their bonds. This lasts until they default, of course. And when they do, the state-chartered banks become insolvent. This is not a failure of the gold standard, or of the free market. It is a failure of a deficit spending policy and central planning.

The most fundamental basis for economics is human decision-making. Satisfying needs and wants creates demand. Engaging in a vocation to provide a good or service of value to others generates supply. The intersection of the two is a market.

Get The Timeless Reading eBook in PDF

Get the entire 10-part series on Timeless Reading in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues.

This week we introduce the unique insight of Mark McElroy. Mark is a friend of 720Global who often provides valuable input on our article concepts, their structure and occasionally challenges their validity. Now, with some minor arm-twisting, he challenges the status quo of economics – the profession, the pedigrees and their intentions.

In Saying It Slowly Doesn’t Help, he doesn’t challenge the PhD economists so much as he takes the rest of us to task. If human decisions are the basis for economics then aren’t we all obligated to be economists at some level? His casual but intentional arms-length observer status poses the question: why is economics so difficult?

Saying It Slowly Doesn't Help

“The quality of ideas seems to play a minor role in mass movement leadership. What counts is the arrogant gesture, the complete disregard of the opinion of others, the singlehanded defiance of the world.” –Eric Hoffer, The True Believer

To communicate about economics is to describe the mirror as if it were a commodity. Economics is a tricky subject. It schemes and dodges—just try to sneak up on a mirror. For all the numbers, parentheses, red and black, boxes and columns, economics is mostly narrative. The digits and bytes of the trade are stand-ins for our resources or assets that are stand-ins for our fears, hopes, memories, hungers and regrets. Economics is the overly eager attempt to hold at arms-length what we don’t want to see up close. Quantifying the narrative is like measuring a joke. But, it must be done. It should be done. Honestly, it needs to be done because no one is alone.

If such twaddle seems impractical, you’re in large company. I get it. That doesn’t necessarily mean you should be off the hook for thinking practically (critically) regarding how we talk about ourselves, our resources, and our guiding principles–economics. Our collective want for information about economics is huge. Really huge. Cable, Twitter, whatever offers a 24/7 stream of info about economics to more and more people. Evidently being in a flood doesn’t make one a hydrologist (that was weak, I apologize). For all the volume of economic info/data available, one would expect we could be fairly proficient in discussing/communicating the basics of economics. Given the rise of six year financing plans for Toyota Corollas, I’m gonna go out on a limb and call BS on the notion that we know how to talk about it effectively. Clearly. Honestly.

If you fancy yourself an economist (and everyone should), it may be of comfort to realize economists are not the only ones in this “we have much to say and struggle to be understood” syndrome. Scientists find themselves there, too. Scientists are studying themselves and the scientific assumptions regarding how to communicate about science. Tired of being picked last for kickball in the public square, scientists are aiming their magnified gaze upon themselves and are coming around to a counter-intuitive notion. The more scientists try to correct and inform the public discourse, the less impact they have. Saying it (you know, smart stuff) with more detail and credentials not only doesn’t work, it makes things worse. Tim Requarth in Slatewrote it like this:

[T]he way most scientists think about science communication—that just explaining the real science better will help—is plain wrong. In fact, it’s so wrong that it may have the opposite effect of what they’re trying to achieve.

I think he meant this:

[T]he way most scientists economists think about science economic communication—that just explaining the real science economics better will help—is plain wrong. In fact, it’s so wrong that it may have the opposite effect of what they’re trying to achieve.

Okay, he clearly did not mean that, but it would have been great if he did. Go read his article in full and play this parlor game. Every time you see “science” or some version of it, replace it with “economics” or some version of it. It pretty much holds up.

Economics should be natural for us to communicate, but it isn’t. Who doesn’t know what a mirror looks like? Economics is discussed ad nauseam as if it were an elusive concept that only a few have glimpsed (yep, just like Bigfoot) when it should be as natural as falling off a bike. Why is that?

I have a guess. Something as simple and natural as discussing the priorities and principles around which we value and exchange our assets has been made complex, confusing, and somehow has justified cable news panels with snooty people using phrases I can’t spell (of which there are many)—all this is the handiwork of a cottage industry (institution) committed to sustaining the confusion for profit, prestige, or because they miss satisfaction of taking names in third grade.

SIDEBAR: I am in a sustained lover’s quarrel with an institution that now spans 30+ years. Institutions of all flavors are the same in that their original spark, purpose or mission always becomes overwhelmed by its desire for self-perpetuation. To be clear, when I refer to the cottage industry proliferating the confusion regarding economics as an “institution,” it is meant as no compliment. If you have finished watching the paint dry and are intrigued by the whole institution thing, check out the work of Eric Hoffer, The True Believer: Thoughts on the Nature of Mass Movements.SIDEBAR CLOSED

If economics remains confusing for me (as is religion and healthcare), I am less likely to experience contentment (or faith or health). Admittedly, though, the institutions that keep economics (and other matters) an ivory tower topic have a willing accomplice in me. It is a co-dependence. Somewhere deep down I need as a way coping for that topic to be at arms-length. At arms-length, I can see economics as a collection of digits, theories, and fractional transactions en masse. I am then spared the need to contemplate the basics of economics: stewardship, community, contentment, and charity.

Honestly, it needs to be done because no one is alone.

Mark McElroy, PhD @B40MKM is a writer, farmer, and management consultant with leadership roles in nonprofit and technology/information companies.

Michael Lebowitz, CFA

Investment Analyst and Portfolio Manager for Clarity Financial, LLC. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director.Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Today is my last official day at the Naval Postgraduate School (NPS) in Monterey. After today, I will be an emeritus professor, with all the rights pertaining thereto. That means mainly I get to use the library, which, by the way, is very valuable.

Get The Timeless Reading eBook in PDF

Get the entire 10-part series on Timeless Reading in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues.

I've enjoyed my 33 years there. That's almost exactly half my life. When I went there I figured that, on a scale of 1 to 10, it would be between 4 and 7. For most of the time, it was between 8 and 9, which is why I stayed.

I later heard, there was a lot of opposition to my being hired.

The biggest draw was the students. They are almost all in the military, either in the United States or in other countries, including, sometimes, Pakistan. The median age is probably about 31. It was actually much easier to get them interested in economics than it was to get undergrads at Santa Clara U, the only place I taught economics to undergrads, interested. I had to work much harder to get the Santa Clara students interested: I succeeded, but I had to work hard.

My experience with teaching at NPS directly contradicted what I was told by the department chairman when I did my courtesy call on arriving there in August 1984. The previous chair had liked me a lot and had hired me even though, I later heard, there was a lot of opposition to my being hired. The new chair had replaced him a month or two before I got there.

His predecessor had hired me on a year to year basis with a handshake agreement that it would go 3 years. When I made my courtesy call, the new chairman gave me some tips about what to do in "your year here." So I knew that he had no intention of renewing. My wife was 5 months pregnant at the time and so I wasn't thrilled about almost immediately looking for a new job.

Early Advice

In my first conversation with the new chairman, he gave me two tips. It's the second one that relates to teaching the students but I want to tell the first one too, because my response to it was key to my turning the chairman around on whether he wanted to renew me.

He said, "There are a lot of people on the faculty who didn't want you here. I don't need to tell you who they are. You'll figure that out pretty quickly when you run into them in the hallway and they try to trip you up."

Earlier on, he told me that if I had any questions at any time, I should feel free to ask.

Most people don't want to think of themselves as liars and so by saying "No," he had to allow that it might really be "No."

I saw my opening. "Bill," I said, "You mentioned that there are people who didn't want me here and who will try to trip me up. I do have one question: are you one of them?"

He paused and then said, "No." "Good," I said, "that's good to know." A year later, he renewed me, and a year after that he supported me in going tenure track. Years later, when I told this story to a colleague in Organizational Behavior, she told me that what I had done is opened up a space in his brain for his answer to be "No." His answer at the time was probably "Yes," but, she said, most people don't want to think of themselves as liars and so by saying "No," he had to allow that it might really be "No." All I knew, at a gut level, was that that was the right question to ask.

His other tip related to teaching. He had read one of my articles in <em>Fortune and, knowing that I was coming from Reagan's Council of Economic Advisers where I had been senior economist for health policy and senior economist for energy policy, he knew that my main interest was in domestic economic policy. He also, I think, figured out that I was a libertarian. He said that if I tried talking about economic policy and tried to elicit the opinions of the students and engage them in discussion, I would get total silence. The students, he said, are professional military, and they are taught not to give their opinions. That seemed strange to me but I'm an empiricist at heart and I resolved to try my approach and see if it worked.

For some reason, I was not trusted to teach a course on my own at first and so was put in to co-teach a class with another economics professor. I'm guessing that he reported back that whatever their worries about my being an ideologue in class, there wasn't much to it. So the next quarter I was given my own class. Finally, l I would get to test the chairman's claim.

Engaging with Students

He was dead wrong. It was easier to engage the students in discussions about policy than it had been at Santa Clara. Each day I taught I would come and say to my wife, "Well, they sure haven't gone silent yet."

He was dead wrong. It was easier to engage the students in discussions about policy than it had been at Santa Clara.

I've actually made their interest part of the pitch my first day of class. I tell them that many of them have seen more parts of the world than I have, that all of them have been in charge of way more people than I have, and that they've probably noticed things that they are curious about. Some of these things, I say, economics can answer. For example, if you've lived in Germany, have you noticed that very few houses and apartments have closets. If you've been to Guam (many of them have – I haven't), what do you notice about buildings in Guam? Sometimes I answer upfront. Other times, I leave them hanging.

Then I say, "To quote from one of my favorite movies, Pocahontas, you'll learn things you never knew you never knew."

A big part of what I teach them is the Ten Pillars of Economic Wisdom. When former students contact me years later, they talk about those things and how they have helped them understand the world. Mike Ward, the new Chief of Staff for NPS, who arrived here last month, said in his first posted statement to the school that he was pleased to make it back here for the retirement of one of his favorite professors: me. He and I went to coffee this week and, sure enough, got talking about the Ten Pillars. Another of my favorite students, a civilian at NASA in Houston, when he found out I was retiring, wrote the following:

I wanted you to know that your class was one that still impacts me to this day. Since that time, I often look at the world through the lenses of the 10 Pillars of Wisdom, and I can say without a doubt that it has been a life-changing experience for me.

The thing I will miss most is being with students over 30 to 40 hours a quarter and seeing, for over 80% of them, the light bulb go on multiple times and with various degrees of intensity.

Sometime soon I'll reminisce a bit about my students' quick humor during class, which is icing on the cake.

About the picture: Terry Rea, the assistant to the Dean, whom I've gotten fond of over the years, put together a PowerPoint presentation showing some highlights of my career. The one at the top was my favorite of her pictures. My second favorite was one of my in an In' N' Out Burger hat. I don't know where she found it.

David Henderson is a research fellow with the Hoover Institution and an economics professor at the Graduate School of Business and Public Policy, Naval Postgraduate School, Monterey, California. He is editor of The Concise Encyclopedia of Economics (Liberty Fund) and blogs at econlib.org.

This article was originally published on FEE.org. Read the original article.

Let’s say you want to be a great gift-giver. If you do, you need to 1) desire the best possible life outcomes for your recipient and also 2) recognize that you don’t exactly know what that best outcome is.

With a healthy regifting economy, gifts flow to their most efficient uses.

All gifts, like all capitalistic ventures, require some risk and leap of faith that you have found the solution to a problem for your recipient, despite all the unknown variables.

It’s also true that most gifts, like most capitalistic ventures, fail to do that.

You should encourage your recipient to feel free to regift your presents. An oven mitt which is useless to Sally (who already has an abundance of oven mitts) may be a perfect gift for her friend Sue (who is just getting started with cooking). One man’s trash is another man’s treasure. Our social stigma against regifting would leave Sue without a good oven mitt and leave a good oven mitt gathering dust in Sally’s kitchen drawer.

With a healthy regifting economy, gifts (like goods and services) flow to their most efficient uses.

You might tell me that regifting is bad because of a loss of symbolic value when you regift something. “It’s the thought that counts,” you might say.

I’m none the poorer for her having given my gift away, and she is actually better off having done so.

I’m not suggesting that you take the positive thought or intention out of your gifts. I’m suggesting that your intentions should include the possibility that regifting and trade is actually a good thing for the recipient, too.

I gave my sister-in-law a bag of coffee beans for Christmas this year. It turns out coffee is not her thing (I didn’t know this), so I encouraged her to re-gift to her colleagues. Coffee beans are a great professional gift, and good professional gifts are great for building social capital and rapport.

She ended up giving the coffee to my Dad, which happened to be a great trade: he had just gotten a coffee bean grinder that same morning. This is a great example of the calculations involved in a regifting transaction. I’m none the poorer for her having given my gift away, and she is actually better off having done so.

In recent years, various scholars have revisited Adam Smith, finding much more in his work than the homo economicus obsession with self-interest. That effort raises important questions — specifically, how might economists incorporate such other moral values as empathy, regard for others, and altruism?

Schapiro and Morson believe that both the humanities and economics could contribute much to the other. The humanities have become too arid and formalistic, they argue; economics has become too “mathematical” and focused on what can be measured than what should be achieved. Their objective is to encourage the unification of the two fields — a Herculean task, certainly, but they take some first steps in that direction.

They criticize economists for arguing that economics alone can resolve policy questions laden with ethical concerns.

Importantly, they recognize that Adam Smith, in The Theory of Moral Sentiments, values the human trait of empathy as equally important to the trait of self-interest he so well explains in The Wealth of Nations. But that emphasis leads them to view these two traits as distinct and conflicting, rather than as interrelated and complementary. Thus, they neglect the ways in which capitalism and its key institution, the corporation, integrate these two traits. A firm must focus on self-interest — how else can it survive? But its employees and managers must also become skillful at “reading” others, at developing the empathetic traits, essential to crafting win/win, mutually beneficial arrangements with its economic partners.

Morson and Schapiro cover an array of ethical issues but give economics greater attention. Specifically, they criticize economists themselves for arguing that economics alone can resolve complex policy questions laden with ethical concerns.

They agree that economics can help managers achieve greater efficiency in achieving their goals; however, they note that the emphasis on analysis and quantitative goals can lead to a neglect of ethics. “Efficiency to achieve what?” is their question. Economists, they assert, have become too “imperialistic,” too quick to convert everything into a quantifiable and solvable equation. But they also note that the humanities have been affected by post-modernist trends, even as they seek to outdo economic imperialism by quantifying the unquantifiable. Their point is that the push toward “scientification” has impoverished both fields, that each should reach out to the other to bolster their capacity to consider ethical questions.

Ethics Are Not Quantifiable, Numbers Are Not Empathetic

While agreeing that complex tradeoffs are involved, they note that too often the ethical issues are ignored.

The utilitarian bias of much economic analysis is certainly ripe for criticisms and Morson and Schapiro add to the work of Deidre McCloskey and others on that score. To illustrate their thesis, they look at an array of policy areas where economics provides a strong focus — admission selection criteria for colleges, markets for kidneys and other organs, and how poor countries might best develop (including a very good review of capital, institutions, technology, and culture). They argue that, while economics often provides guidance on how to “efficiently” address such problems, too often it runs the risk of failing to attain richer and more ethically grounded, but less readily quantified, objectives.

Their example of college admissions provides a detailed discussion. The authors — both full professors and one the Dean of Northwestern University — are well equipped to address that area. They understand the costs of over- or under-fulfilling enrollment goals. However, they warn that too often admissions officers neglect the moral and ethical challenges that prospective students face. Is it ethical for colleges to use variable pricing based on a student’s likelihood of acceptance to provide them less financial aid? Businesses, of course, use diverse price levels of necessity, but should colleges? Is their goal to educate or maximize their students’ lifetime achievements? And if so, is that interpreted in earning potential or some other metric?

While agreeing that complex tradeoffs are involved, they note that too often the ethical issues are ignored. They suggest that while university spokesmen claim to speak with moral authority, their marketing policies are more akin to those of used car salesmen.

Not Always On-Point

However, when the authors turn to areas outside their core competency, their discussion is less insightful. The discussion of the ethics of allowing markets for organs, kidneys specifically, recognizes the limits of donations based on familial or friendship ties. Tens of thousands of individuals in need of kidney transplants remain on waiting lists every year. They discuss some innovations — such as chain donations that give a donor the right to a kidney for themselves in the future — and they recognize that allowing compensation might eliminate the deficit. But they worry (as do scholars such as Harvard philosopher Michael Sandel) that confronting individuals, especially the poor, with such market choices creates avoidable ethical challenges.

A true understanding of Smith’s insights — and capitalism itself — requires a larger perspective.

What “should” or “should not” be in the market — from payday lending to kidney transplants — is an ongoing debate, but I do not view that as a conflict between an ethical and a utilitarian choice. Rather, such “economic” transactions, being cooperative and benefiting both parties, are also altruistic.

Morson and Schapiro seem to realize this point, at least in part. In their chapter, “De-hedgehogizing Adam Smith,” they note that Smith wrote extensively about ethics in The Theory of Moral Sentiments, arguing that self-interest, a trait critical for human survival, is balanced in social interaction by the other-regarding trait of empathy, or “fellow-feeling,” and that the market is made possible only by the creative synthesis of these two traits. Competition provides the discipline to keep the two traits in balance. Both are necessary for the creative voluntary system of wealth creation that is capitalism in practice.

A true understanding of Smith’s insights — and capitalism itself — requires a larger perspective. Thus, a dialogue between two large and complex fields of knowledge seems a useful, though difficult starting point. Still, this book may still encourage others to open the door to a broader understanding of the morality of markets and capitalism. On those grounds alone, it merits attention.

Fred L. Smith, Jr. is the founder of the Competitive Enterprise Institute. He served as president from 1984 to 2013 and is currently the Director of CEI’s Center for Advancing Capitalism. He is a member of the FEE Faculty Network.

This article was originally published on FEE.org. Read the original article.

Valuation-Informed Indexing #395 on how stock investing works and its connection to Adam Smith and Eugene Fama

By Rob Bennett

Buy-and-Hold is “sticky.” It is my view that Robert Shiller’s 1981 research showing that valuations affect long-term returns discredited the efficient market theory, which is the core belief of the Buy-and-Holders. So Buy-and-Hold should have passed from the scene by now. At the very least, we should see it being challenged everywhere it is promoted.

But that is not even a tiny bit the case. Few investors are dogmatic Buy-and-Holders. But the vast majority believe at least somewhat in the core principles of Buy-and-Hold. When a newcomer to investing goes looking for a simple description of the basics of stock investing, he is almost certainly going to be told some version of the Buy-and-Hold story. The Buy-and-Hold model for understanding how stock investing works remains dominant today.

Why? I need to have an answer to that question. I would like to see Valuation-Informed Indexing (the model rooted in Shiller’s research rather than in Fama’s) become dominant. This does not seem even close to happening 37 years after Shiller published his “revolutionary” (Shiller’s word) research findings, research that caused Shiller to be awarded a Nobel prize in 2013. What’s going on?

The biggest reason is that Buy-and-Hold tells investors that their portfolios are worth more than they really are at times of overvaluation. We have been at very high price levels for over two decades and investors naturally enjoy being told that their accumulated wealth is greater than it is. So it is understandable that Valuation-Informed Indexing has not caught on with the general population of investors.

But how about with the experts? Experts in this field obviously follow developments in the peer-reviewed research. They know about Shiller’s Nobel prize. They understand that their job is not to tell people what they want to hear but to offer informed views as to how stock investing works in the real world. Why are there not more experts singing the praises of Valuation-Informed Indexing and warning of the dangers of Buy-and-Hold?

I think that a big reason for the delay in the spread of Shiller’s ideas is that the alternative to Shiller’s model — Buy-and-Hold — has roots that go very deep. Eugene Fama is the economist who did the most to lend theoretical support to the Buy-and-Hold Model. But the general way of thinking about how money transactions work that informs the Buy-and-Hold Model really began with Adam Smith and Adam Smith’s ideas inform the thinking of every economist alive. When an economist is asked to question his belief in Buy-and-Hold, there is a very real sense in which he is being asked to question his belief in things he learned in the first textbooks on economics that he ever read.

It was Adam Smith who promoted the concept of a “Rational Man” who makes the economic choices that best advance his self-interest. Isn’t that what Buy-and-Hold is all about? Buy-and-Holders believe that the market is efficient, that is, that it is always properly priced. Why is the market properly priced? Because we are all acting in our self-interest. If some of us noticed that the others of us had priced stocks improperly, we would swoop in and exploit the mispricing to our benefit. The reason why Buy-and-Holders believe that it is not possible for market timing to work is that one can successfully time the market only by outsmarting it and it is hard to imagine how anyone could be smarter than a market of millions each acting rationally in pursuit of his or her self-interest.

Shiller is saying something very different. He is saying that it is shifts in investor emotions, not economic realities, that are the primary drivers of stock price changes. Investors who permit emotion to steer their investing choices are not acting in their self-interest, they are acting irrationally. Of course they are not even aware that they are failing to act in their self-interest. In the Shiller model, investors hurt themselves by giving in to emotional impulses to push stock prices ever higher and individual investors who possess the ability to see through the irrational exuberance can indeed profit by being smarter than an overall market that is not very smart at all,

This is a big, big, big, big change in perspective. The question of what causes stock price changes is fundamental. And the implications of Shiller’s Nobel-prize-winning findings are far-reaching indeed. If Fama is right, the stock market is a safe place to put one’s retirement money given that human reason rules the day under this understanding of how the market works. Shiller’s vision is a frightening one to someone with a longstanding belief in Adam Smith economics. If Shiller is right, the numbers on our portfolio statements do not reflect hard economic realities but only the passing fancies of millions of emotion-filled investors.

An economics professor once told me that I should not expect to see Valuation-Informed Indexing gain serious ground on Buy-and-Hold until we experience a “paradigm change,” something that probably can only be brought on by a deepening economic crisis. For experts in this field to give up their confidence in Buy-and-Hold, they have to question things that they have subscribed to as basic truths for as long as they have been earning a living doing work as economists. Shiller’s ideas challenge everything that we once believed about how stock investing works. That’s why they excite me so. But that’s also why they face such a struggle gaining a foothold among the experts and ultimately among the general population of investors.

Last week it was reported that the illinois Budget was in dire financial straits making it a perfect candidate for Sate Bankruptcy. The state faces $15 billion in backlogged bills and mounting ratings downgrades from credit agencies. The struggling state is poised to obtaining the dubious honor of being the first state to be rated junk status in US history. Traders have responded in kind sending the yields on Illinois bonds higher-a reaction from court orders that claim the state violated previous orders and must adhere to prior obligations to vendors.

The State has yet to pass a budget for the last three years – the longest for any US state- and has recently announced via its Transportation Department that roadwork would stop starting July 1st. The Powerball lottery is also considering dropping Illinois over its lack of a budget. Compensation to state employees is in jeopardy of evaporating. According, to a recent piece from the Associated Press, the state Comptroller Susan Mendoza is sounding the alarm regarding the turmoil the financial strapped state is facing. The piece explains that court ordered lawsuits by state suppliers are binding but the state’s monthly revenue isn’t enough to meet these obligations. This puts services such as school buses and ambulance services at risk of shut down.

In the state legislator, both parties are battling over the finances of the state. The Governor, Bruce Rauner, has been adamant about instituting changes to the budget before supporting any tax increases. Democrats in the State argue that his demands like term limits for lawmakers, a four-years property tax freeze, and new worker compensation laws would hurt working families. Such arguments will fall on deaf ears as the State increasingly faces the harsh reality of mounting bills coming due. State suppliers and vendors are increasingly lining up to file lawsuits against the state demanding payment. Recently, The administrator for the State’s Medicaid program went to court to obtain a order for $2billion of unpaid bills. The city is running out of time and drastic measures are needed urgently for the Illinois budget. “Once the money’s gone, the money’s gone, and I can’t print it,” Mendoza said.

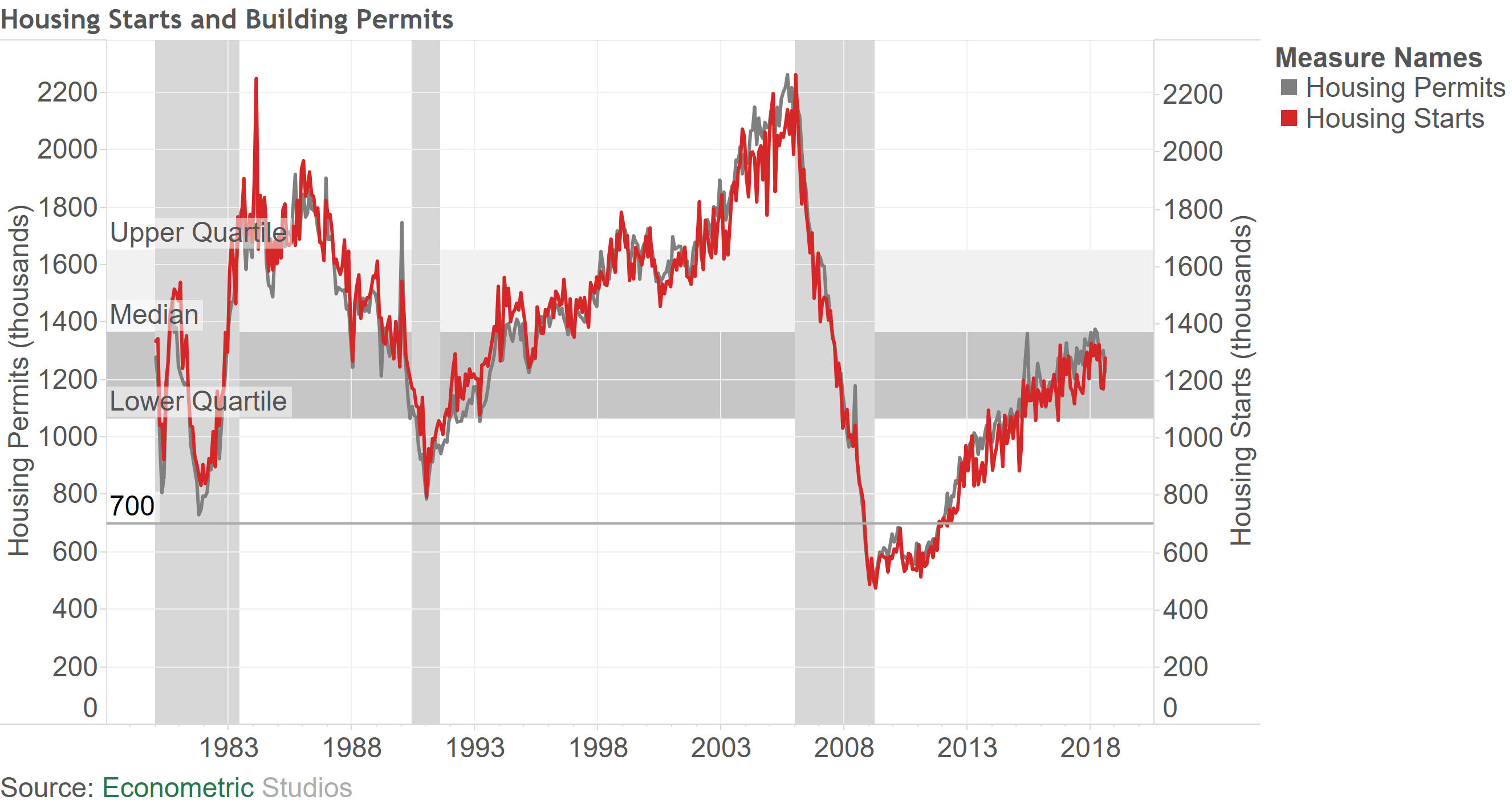

Housing took center stage this past week. Housing starts, new and existing home sales, and Case-Shiller home prices gave us an idea of what the American housing market looks like.

Question: If you had to guess what stage of the business cycle the housing market says we’re at, what would you guess?

The economy has been expanding for just over 9 years now. Perhaps this would indicate we’re close to peaking? Then again, the younger generation has been slow to take part in the housing expansion, so maybe we’re in the middle of an expansion? Household formation has been quite strong of late, maybe this would say we’re just starting to enter another housing boom?

First up, housing starts. Housing starts came in at 1.282 million, an increase of 108,000 over July’s figure. Since bottoming at 478,000 in April 2009, housing starts are up 804,000.

The median housing starts figure since 1980 is 1.366 million.

The prior two recessions saw housing starts peak at 1.972 million and 2.273 million.

How long until housing starts reach say 90% of the 1.972 million figure? At an average monthly gain of 8,000 per month (what we’ve seen this expansion), that’s 62 months, or just over 5 years. That puts us in 2023 for the next recession.

New & Existing Home Sales

The shorter of the two measures, Existing Home Sales peaked at 5.5 million prior to the 2001 recession. Existing Home Sales provided no lead time in this case. In contrast, Existing Home Sales peaked at 7.3 million in 2005, 2 ¼ years before the formal 2008/2009 recession began.

The most recent figure, 5.4 million for August 2018, is in murky territory. No indication here. Of course, if one divides Existing Home Sales by the number of U.S. households, there picture is more positive. As of now, Existing Home Sales per household is not booming, nor deteriorating.

New Homes Sales to households provides a clearer picture. The measure at 426 is below any prior measure prior to a recession. The measure peaked 2 ½ years at 1,182 prior to the 2008/2009 recession. The lead was also 2 ½ years prior to the 2001 recession. The lead was 5 years prior to the 1991 recession.

Taking the average of these 3, the next recession is in early 2022.

Case-Shiller Home Prices

Lastly, the Case-Shiller home prices. Of the 20 cities reported, 10 have surpassed their housing market boom. Some are way past their prior peak, such as the über-booming Dallas-Fort Worth, Texas area.

Some cities are really booming, and probably need some of a breather. Other cities have many years of expansion left in them.

Summing Up

If one looks at the lead time housing starts, existing home sales, and new home sales provide for the economy, the 3 measures are saying the economy has at least another 3 years until a recession, and perhaps another 5.

If you like the articles and would like access to all the raw data and visualizations behind our articles, please subscribe.

Nobel Laureate Robert J. Shiller is Sterling Professor of Economics, Department of Economics and Cowles Foundation for Research in Economics, Yale University, and Professor of Finance and Fellow at the International Center for Finance, Yale School of Management.

In this exclusive Network Capital Premium masterclass, he reflects upon his career and shares precious advice for students and young professionals. In this riveting discussion, you will learn about his life, his mental models and collaboration principles.

Get The Full Warren Buffett Series in PDF

Get the entire 10-part series on Warren Buffett in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues

Robert Shiller: Lessons In Economics From Samuelson's Textbook

Transcript

Dr. Shiller, welcome to network capital. It's an honor to have masterclass by a Nobel laureate. We appear to be a skill sharing community and are very interested to learn more about your career. Let's start from the beginning. What got you interested in the subject of your work.

It's hard to remember. I first guy interested in economics, I think, when my older brother came home from college with this Samuelson economics textbook. I have a tendency to pick up things to read them and I read that Samuelson's textbook. So it got me going.

And in school and college student member how life was studying economics like or did you really relish the subject or was it hard at times.

First it was hard at times. Did I relish it? You know i could have I majored in anything, I can be a professor of you name it. I wanted to be a scholar at that age but I didn't necessarily focus on economics. I thought maybe people that I met that who impressed me. Philosophy [inaudible] economics is been called worldly philosophy that was from worldly philosophers was the title of the book.

It seems Adam Smith was a professor of moral philosophy maybe that appealed to me.

So at what we're talking about right now? What did you [inaudible] scholar?

I just moved up from age 14 when I read Samuelson's textbook to age 19 when I began to really focus on the idea of economic career.

Wonderful. And what, at that time was that a question or a set of questions that you wanted to solve with the economic lens? Because you mentioned that you wanted to be a scholar and not necessarily a scholar in economic. So what questions were you thinking about?

Well economics impressed me as it solves real problems. It has a technology for solving. I would add finance to it, that is a subset of economics. Samuelson said, In think in his text book. I try to remember, its been a long time. But it seems that I believe this is a very lose memory of him. I believe in economics and promoting the wealth of people because it matters to real people things like health care education, they transform our lives. There are many different single problem but the overall problem is developing the economy and improving the standard of living and allowing people to make choices that matter about things that matter to them.

How was undergraduate education for you? Did you find some mentors in college?

I did find mentors in college. What comes first to my mind was Kenneth [inaudible] I went to the University of Michigan which was a major state university in the United States. Kenneth {inaudible], he presented a view of economics that was highly morally grounded in fact just after I graduated he gave the presidential address before the American Economic Association entitled, "economics as a moral science". I was in Chicago, if I remember, I may be wrong. It was 1969. But I went to hear his speech. He is my former teacher.

What he said that economics particularly allows us to invent the world that we live in and it should be done with a moral purpose that particularly impressed me. [inaudible] Faculty members who impressed me a lot. One of them was a history professor Shaw Livermore. Maybe I haven't heard much about him. He gave a course that talked about the Great Depression and why it happened.

Feb. 7, 2020 Update: As of midday, the Russell 2000 (INDEXRUSSELL:RUT) is trading down by about 14 points or 0.82% at 1,663.74. The small-cap index pulled back alongside the S&P 500 and the Nasdaq Composite as the stock market in general retreated. The Russell 2000 is down approximately 2% for the week and continues to struggle.

Cantor Fitzgerald and Susquehanna Financial Group analysts are both writing about the INDEXRUSSELL:RUT this week. They both suggest using options on the iShares Russell 2000 ETF, but they disagree on whether it’s time to be bullish or bearish.

Bearish options on the ETF have gotten cheaper than bullish contracts after the stock market rallied earlier this week. Stocks pulled back amid fears related to the coronavirus. However, those fears started to rise again today, which is why the Russell 2000, S&P 500 and other stock indices pulled back.

Hedging with the index

Cantor Fitzgerald strategist Peter Cecchini is advising investors to re-hedge using options on the Russell 2000 ETF. He noted that volatility has come down a lot since the first selloff from the coronavirus. However, put-spread payouts have again climbed one standard deviation over their mean.

Susquehanna analysts are bullish on the INDEXRUSSELL:RUT fund, however. They note that the $160 level served as a key resistance level for much of 2019. They now see that level as a new support level and believe the iShares Russell 2000 could be moving even higher.

If fears about the coronavirus and other international issues continue, it is possible the Russell 2000 will stage a comeback. Analysts say it could outperform its large-cap counterpart, the S&P. This is because investors might seek safety in small-cap names. On the other hand, investors have long been showing their preference for big companies as the S&P has been outperforming the small-cap Russell 2000.

Investors simply treat small-cap and large-cap companies differently. For example, they may be more accepting of an earnings miss from a company whose products they know and use. One concern for small caps is that their costs have been rising faster than demand, according to Nordea Asset Management strategist Sebastien Galy. Large-cap companies, on the other hand, can more easily absorb such costs.

What is the Russell 2000 (INDEXRUSSELL:RUT)?

The Russell 2000 (INDEXRUSSELL:RUT) is a stock index used as a measuring stick for small-cap companies. It provides a quick glance at how smaller companies are doing, compared to the S&P 500, which includes the 500 biggest large-cap companies. The companies that are included in the Russell 2000 have market capitalizations that are much smaller than the market capitalizations of those included in the S&P 500.

The index is a subset of the Russell 3000, which is made up of 3,000 of the biggest stocks in the U.S. The Russell 2000 (INDEX:RUSSELL:RUT) consists of about 2,000 of the smallest-cap stocks included in the Russell 3000.

As of Feb. 7, 2020, the Russell 2000’s all-time closing high is $1,740.75, which was set on Aug. 31, 2018. The index’s all-time intraday high is $1,742.09, which was set on the same day as the record closing high. In 2019, the index posted a price return of 23.72% and a total return of 25.52%. For comparison, the large-cap S&P 500 returned 31.49%, including dividends, and climbed 28.88% in 2019.

Why is it important?

The Russell 2000 (INDEXRUSSELL:RUT) is an important benchmark. It is utilized by mutual funds and hedge funds that trade a lot of small-cap stocks. Funds use it to compare their own performance to that of the index. The index serves as a sort of measuring stick so funds can check how they did against a group of stocks that’s of comparable size to their holdings.

Many also see the index as an important indicator of how the U.S. economy and smaller businesses are doing. The constituents of the Russell 2000 are seen as domestic because they receive more of their revenue from the U.S. For this reason, news headlines that affect international markets may have less of an impact on the Russell 2000 than on large-cap indices like the S&P.

Investing in the INDEXRUSSELL:RUT

There are several ways to invest in the Russell 2000. You may consider investing directly in some of its constituents. However, there are also broader ways to invest, like with an exchange-traded fund (ETF) that tracks the index passively.

Some popular ETFs that track the INDEXRUSSELL:RUT include the iShares Russell 2000 ETF and the Vanguard Russell 2000 ETF. Other options for investing in the INDEXRUSSELL:RUT include buying options and index futures.

In 2019, several stocks outperformed the Russell 2000 Index. Some of the stocks that pushed the index and the ETFs that track it higher in 2019 include EverQuote Inc., ConforMIS Inc., Digital Turbine Inc., Achillion Pharmaceuticals Inc., and Kodiak Sciences Inc.

Say that you own a bowling alley. You need to make decisions about how many employees to have on staff next year and on how much money to direct to advertising and on how much you can charge per game and still expect to be able to earn a profit. There are lots of places to which you can turn to get the information you need to help you make these decisions. You have your records from last years. You have data on demographic trends in your area. You have journals in your field reporting on how bowling is becoming a more or less popular entertainment option.

There’s one source of information that you need to take into consideration but that you might not think to consult: Robert Shiller’s book Irrational Exuberance.

Get The Full Ray Dalio Series in PDF

Get the entire 10-part series on Ray Dalio in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues

That’s an investing book! What can an investing book reveal about how to run a bowling alley?

It can reveal a lot. The title of Shiller’s book is profound. When he describes stock market gains above those that would apply if the market were priced properly as the product of irrational exuberance rather than as the product of a rational assessment of economic realities, he is saying that those amounts are not real. Stocks are today priced at two times fair value. So Shiller is saying that half of the money that today’s investors are counting on to finance their retirement represent nothing more than cotton-candy nothingness fated in time to be blown away in the wind.

Changes In The Popularity Of Competing Entertainment Options

That’s a reality with far-reaching economic implications. If half of the money in our stock portfolios is going to disappear (irrational exuberance has always eventually disappeared during the 150 years of stock market history for which we have good records), we are not going to have as much money to devote to discretionary entertainment expenses like bowling. The loss of that money will have a bigger effect on how many people go bowling in the future and on how much they will be willing to pay to do so than demographic changes or changes in the popularity of competing entertainment options like going to the movies or enjoying a casual dining-out experience.

The proprietors of bowling establishments consider demographic changes and changes in the popularity of competing entertainment options when making decisions as to how to run their businesses. They do not take Shiller’s research findings into consideration. Why?

Shiller’s research findings represent a revolutionary change in how our economy works. In pre-Shiller days, we thought of the numbers listed on our portfolio statement as real. They sure seem real. If you ask to cash in your stock holdings, you will be paid the full amount listed on the statement. That suggests that those numbers are pretty darn real, does it not?

Shiller is saying otherwise. He is saying that some of your stock portfolio is real, the amount that reflects the fair-value price for the stocks you hold is real. But he is also saying that the amount by which the nominal value of your holdings exceeds their fair-value price is the product of irrational exuberance and not real and lasting but fake and temporary.

The Irrational Exuberance Factor

It’s tricky knowing when to take the irrational exuberance factor into consideration when running a business. It can take 10 years or more for irrational exuberance to disappear. So, if you make business plans based on the irrational exuberance present in the market price today, those plans may be off the mark. The other side of the story, of course, is that, if you make plans that ignore the irrational exuberance factors, your plans may be even more off the mark. The most prudent course of action is to accept that the risk of the disappearance of the irrational exuberance is greater the more that stocks are overpriced and the longer that they have remained overpriced while also understanding that precise predictions of when the disappearance of irrational exuberance will come to have economic significance are not possible.

The issue here of course applies to all businesses, not just to any one bowling establishment. When people see a large portion of their life savings disappear, they spend less. When stock prices fall hard, we all see a large portion of our life savings disappear. All of us who care about the ongoing success of U.S. businesses should be doing what we can to insure that stock prices never get so high as to make the sudden disappearance of a large amount of irrational exuberance a likely possibility.

Risk and reward in the age of the COVID-19 pandemic by Harry Friedberg, partner, BX3

The concept of risk and reward is ingrained in all facets of life. Of a new product launch with an aggressive roll-out date, we’ll say “no risk, no reward.” At the baseball diamond, when the coach gives the sign to steal home to win the big game, we deem it “worth the risk.” It would be my guess, however, that we never really think deeply about the actual meaning behind these phrases. What exactly is risk-reward and how do we come to these conclusions?

In simple terms, we are making a calculated bet where outcomes can be ascertained and after analysis of all the possible outcomes relative to the goal or reward that can be achieved, we deem that it would be an appropriate measure to go forward with a plan, task, or investment.

In normal environments, one is able to make assessments of possible outcomes. This isn’t to say that there is certainty of these outcomes but rather, that there is a certainty to the possible uncertainties. Market data, experience, and the sound advice of professionals enables you to decide all of the possible outcomes, then assign a percentage of likelihood. Let’s use a new product introduction as an example. The percentages for likely outcomes may look like this:

Unprecedented product adoption with no modifications: 10 percent

Moderate success of product: 25 percent

Product requires substantial additional enhancements and expenditures: 10 percent

Market reception is mixed, not much added to incremental revenues: 28 percent

Market is yet undefined and product fails: 25 percent

Product fails, marring reputation of company and existing products: 2 percent

Monte Carlo Simulations

The best course of action in this case appears to be doing more market research and product development before deciding to roll out the new product—a course of action that may seem conservative, but one that is supported by the likelihood of the various outcomes. These calculations are known as Monte Carlo simulations. Consciously or unconsciously, all individuals, investors, and businesses make these calculations each and every day.

With the world grappling with unprecedented uncertainties, individuals, companies, and investors are now trying to figure how to factor in an ever-increasing array of possible outcomes. Ideas once thought of as absurd or impossible, are suddenly considered possible, if not very likely. In recent days, I have had people ask me about the likelihood of some of their thoughts and fears, such as “What happens if people don’t fly on planes for three months or more?” or “Can we survive if not one person comes to our restaurant for a full month?” or “What happens if people never go out again to shop and instead order everything from home?”

Until risk takers of all sorts can come to some sort of conclusion as to what to expect, action becomes impossible. In the present private equity environment, this is freezing up investments. Until probabilities can be calculated and a course of action can be deemed the appropriate risk-reward, inaction seems to be the best action.

Alternative Assets: Life’s Been Good Pre-COVID 19 Pandemic

But there is more danger that private equity investments are facing than just uncertain times. If I can borrow from the immortal words of musician Joe Walsh:

In the pre-COVID-19 days, the early-stage, speculative nature and relative illiquidity of a private equity investment was balanced out by the potential of outsized returns relative to more liquid investments like listed stocks or bonds. As a case study, let’s take XYZ Co., which has a new, unique software application. Sure, it was in the process of revolutionizing the world while waiting to be validated by the market, but when — let’s think positive here — it is successful, an investment in XYZ would offer outsized return relative to any puny old listed stock or bond of a more established company.

Now, however, with stocks down more than 30 percent in just a few weeks and bond yields of formerly high-quality companies soaring, investors can look elsewhere for high returns. Take the fixed-income market: Bonds that not too long ago were yielding less than 4 percent, are now approaching 10 percent. That means it’s harder for private equity to stand out. On a relative basis, PE, venture capital, hedge funds and indeed all investors are weighing where is the best bang for their buck.

So, what does this mean for private deals today? For starters, if they hope to attract any attention with investors in today’s environment, debt deals need to consider contributing more equity kickers, and private equity investments need to rethink their valuations. It’s just that simple. Investors are financially driven. We know that. At times, however, founders can get so focused on their vision that they forget that money is the ultimate motivator for investment. Investors are always considering relative returns. If a more liquid, listed alternative is offering outsized returns, for at least the short term, those instruments will be the focus of most private investors.

Asset Class Performance Prior To The COVID-19 Pandemic: Honey, Haven’t We Seen This Show Before?

Does this mean private equity is irrevocably changed? Do all founders need to accept that this is the new reality? If this is the new reality, how can private equity even compete?

The short answer is that we all need to catch our collective breaths. The famous last words of any investor are “this time it’s different.” While the COVID-19 pandemic does present some scary times and uniquely different challenges, the short-term flux will definitely be disruptive to private equity, but not forever. The silver lining is that we will eventually return to normalcy.

How can I be so certain that we will return to a stable normalized market? Well, being a financial professional for 32 years, I have seen my fair share of cataclysmic market disruptions: the Black Monday crash of 1987; the Russian ruble crisis of the mid-90s; the late-90s Asian financial crisis; the early 2000s dot-com bubble; the market disruption following the attacks of September 11, 2001; and the late-2000s Great Recession, to name just a few. After each of these events, the world felt irrevocably changed. In many ways, it was. But the financial markets persevered.

Did it take some time to rebuild, to feel confident enough to evaluate risk and make intelligent, well thought out bets again? Absolutely. Yet after each crisis, we learned a little bit more and we came back stronger. Prior to the COVID-19 pandemic, private equity investments were at record levels, even with all the crises occurring in our past. Given time, we will no doubt surpass those levels.

We Need To Stabilize The Markets

First, however, we need to stabilize. We need to be able to properly analyze risk-reward again and for that, we will need some clarity. Investors will no doubt pursue public investments, but that pursuit will eventually drive them back to levels where they no longer compete with the returns that private investments offer. In short, we need to be patient.

In the meantime, there is a lot we can do together to strengthen our standing when markets stabilize and liquidity returns. Founders should continue to drive their innovation forward, hone their stories, conserve cash, and continue making connections that strengthen their business. They need to be mindful of the world around them and understand that investors have a lot of balls to juggle. There are plenty of ideas that can still get traction but for all of us, patience and collaboration are the keys to help each other through these difficult times.

For our part, we need to continue to help offering guidance to our clients, to point out government programs that will help fund their small business during this uncertainty, to offer services that can help keep the ship afloat—not for profit, but for the good of our clients. Getting the word out on the great things our founders are achieving and raising their voice above the din of difficult times will better position us all for the inevitable, better tomorrow yet to come. Most importantly, we need to understand that we will go down this road and succeed if we all work together. To me, that risk is worth the reward.

In a post last week (Maybe COVID-19 Won’t Be That Bad), I wrote that the impact of the virus in terms of deaths and strain on American hospitals looked like it might be less than what was feared. Developments over the last week have supported that view. The Institute for Health Metrics and Evaluation at the University of Washington further lowered its estimate of U.S. COVID-19 deaths from about 82,000 to about 62,000 by August.

The Virus

Get The Full Ray Dalio Series in PDF

Get the entire 10-part series on Ray Dalio in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues

Screen capture via the Institute for Health Metrics and Evaluation.

Similarly, it now looks like we're on track for about 27,000 deaths by April 15th, rather than 37,000. And, as you can see in the screen capture above, as of Sunday night, the growth in the number of deaths and the number of new cases were both in the single digits, while the growth in patients recovered from the virus was above 30%, all hopeful signs that we may be past the peak of the virus. The economic news will likely get a lot worse though.

The Economy

No economic downturn in America since the Great Depression has been called a depression, but if an economic decline of 10% counts as a depression, and J.P. Morgan predicts a 40% decline in GDP in the second quarter, it's hard to see how this isn't a depression. Economist Justin Wolfers estimated earlier this month that we're already at 13% unemployment, which would be the highest unemployment rate since the Great Depression. Wolfers said unemployment could be rising at half a percent per day, which would be consistent with St. Louis Fed President James Bullard's prediction last month that it might hit 30%.

The Market And Your Security Selection Method